There are many rules of thumb out there when it comes to life but what I want to write about are the most important ones that deal with money and getting rich. I love and rely on rules of thumb that help guide me in many facets of my life, especially managing my finances.

A rule of thumb is a term for practical advice, a guiding principle based on theory or experience simplified enough to follow it (if we choose to) and yield success.

What if we have the most critical rules of thumb about money to help guide us? I collected the financial rules of thumb passed on by family, friends, experts, and successful, wealthy individuals. These rules of thumb are invaluable to remember and apply in our lives.

Many of these rules of thumb can be thought of as a starting point to help align ourselves to the application of the rules and methods for financial success. In addition, it can help us assess our current state and help us find the route to where we need to be to become financially well-off and thrive in our financial life.

Without further ado, here are the most valuable rules of thumb in money and wealth that will make us rich if we follow the advice consistently.

One of the most significant lessons I learned from the 1926 book “The Richest Man in Babylon” by George Samuel Clason was the key to building wealth was to pay yourself first.

When we pay ourselves first instead of last, we can always keep what we earn at a constant rate and continue to accumulate it no matter what. As I have written before, there is a reason why the U.S. government takes its cut for taxes first in our paycheck. It is ensuring itself that they are paid first.

We can alleviate this by ensuring we pay ourselves first before the government takes its cut. One way to do this is to set aside 10% or more of our money to save for retirement or savings. This method could be done via participation in our company’s 401K or Traditional or Roth IRAs. The beauty about 401Ks is that often our employers have a percentage match, which is like free money they provide for us to invest in our retirement. In addition to our 10% or more set aside, we can ensure we pay ourselves first.

By paying ourselves first by setting aside for retirement, we also lessen the taxable income the government can take from our paycheck, ensuring that we keep as much of it for ourselves as we want.

“I found the road to wealth when I decided that a part of all I earned was mine to keep. And so will you.”

“A part of all you earn is yours to keep. No matter how little you earn, it should be less than a tenth. It can be as much more as you can afford. “

— “The Richest Man In Babylon” by George Samuel Clason

The rule is that we should pay ourselves no less than 10% of any income. For example, if we make $100, then 10% of that should be saved, which is $10. We should always do this for any earnings, and the next thing is – we should not touch it unless we have to, meaning we need to save, accumulate, and let compounding interest do its job to make that money work for us.

Compound interest is when the interest of what our money earns starts earning interest. In summary, our investment can accumulate and compound if we let it. If we save our money in a financial vehicle that makes a high-interest rate, such as stocks, real estate, and other high-bearing interest rates financial methods, we can see our money double as time goes by.

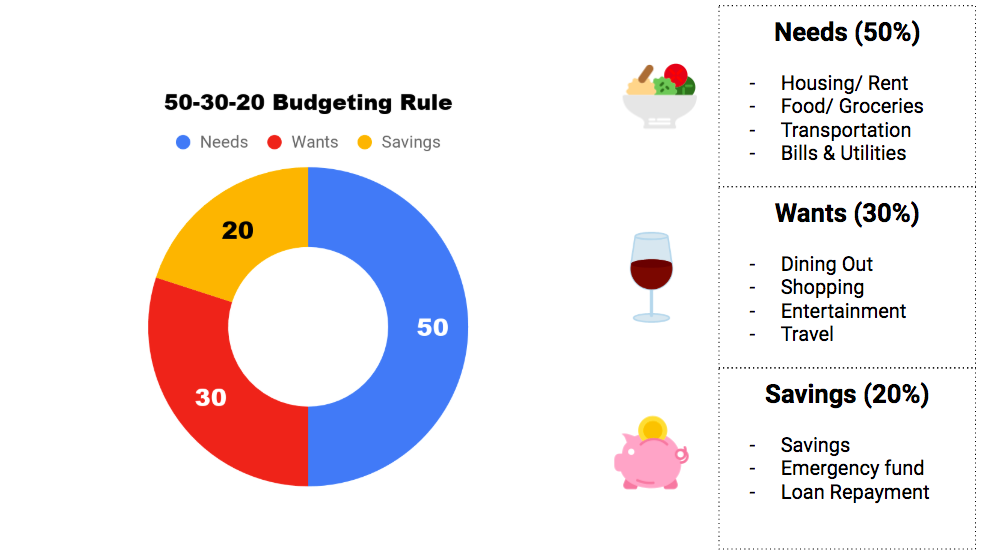

The 50/30/20 rule is an easy rule-of-thumb method for budgeting to ensure we manage our money effectively. The rule starts by using our monthly after-tax income and allocating these into three spending categories, 50% of that money should go toward needs, 30% should go towards the “wants,” and 20% should go towards savings or paying off any debt.

We can create a streamlined budget when we keep our income and expenses balanced by budgeting and simplifying our spending areas into 3 main parts. A simplified budget ensures we can follow it consistently.

The success of this rule of thumb boils down to specifying the three main spending areas correctly.

The 50/30/20 rule of thumb is an excellent way to create a budget and streamline our financial goals.

The COVID-19 pandemic was one of those extreme situations we thought we would never encounter, but we did, emphasizing the importance of an emergency fund.

An emergency fund is the rainy day fund we use when we need money, such as when we become unemployed or when a disaster strikes. We need to spend the money to help us navigate and overcome that situation.

On unique circumstances, for example, would be an expense we did not plan for, such as repairing our car or patching our roof all of a sudden. These are events that are often outside of our control. Having an emergency fund helps us shoulder these events and protects us financially.

The rule of thumb when starting an emergency fund is to start small. We should first start with at least $1,000 of an emergency fund set aside. This money should reside in an account we never touch and only reachable to us in an emergency. For my personal use case, I have a separate online bank account where I save my emergency fund. The idea is that an emergency fund should be liquid and available immediately.

The rule of thumb for how much a good emergency fund amount is would be at least 6 months of living expenses. We define expenses as the “needs” expense which includes our rent or mortgage, our food, our utilities, and other areas of the expense we need to live day-to-day. We add all of these expenses and multiply by 6 months or more. So, for example, if we need $3,000 to get by for a month, multiplying that by 6 months yields an emergency fund of $18,000.

We can slowly build up to this total amount, but it is paramount that we do have it – there are many uncertainties in life, and an emergency fund is our insurance, so we are not left helpless during a rainy day.

This emergency fund of at least 6 months is a great way to help protect ourselves and our families and ensure that we meet our future financial goals amid uncertainties.

I have written about the lessons I learned from the book “The Millionaire Next Door” by Thomas J. Stanley and Willam D. Danko, where a study of millionaires and their habits showed surprising learnings about how to get rich. One major lesson in the book is that real millionaires track their net worth closely.

We can define net worth based on what we own, our assets minus what we owe, our expenses, and our liabilities. The book “The Millionaire Next Door” has a formula for assessing whether we are great wealth accumulators. The formula is 10% x Age x Income = Expected Net Worth.

So, for example, if we are 30 years of age with a $100,000 yearly income, our expected net worth should be as follows: 10% x 30 x $100,000 = $300,000. This means a great wealth accumulator should have saved about $300,000 at age 30, making $100,000 a year. If the amount is less than this, then it is likely that they could be better at accumulating wealth.

The rule of thumb for net worth is a great indicator and tracker of how we are doing with our financial goals. If we decide to become wealthy, we must work on tracking our net worth and increasing it through either savings or accumulating assets.

We must also decrease the expenses and liabilities. These could include mortgage payments, car loans, and credit card debt. We increase our net worth when we work to control and minimize our expenses and liabilities.

The oracle of Omaha, Warren Buffet, invented the 90/10 rule of thumb strategy for investing. This method of investing describes putting 90% of the investment into stock based on the index fund, such as the S&P 500, and the remaining 10% towards a low-risk investment, such as U.S. government bonds.

This strategy aims to generate a high yield in the overall portfolio for investing long-term. Again, this method works for long-term investments of 10 years or more, but it is an effective way to build wealth automatically.

The 90/10 rule is a recommended benchmark that could be adjusted. Perhaps based on risk aversion, it could be changed to an 80/20 or other, and it could also change over time as we move closer to retirement, when we must preserve most of that money to take out for our living expenses.

For more information on the 90/10 rule of thumb, Investopedia [https://www.investopedia.com/terms/1/90-10-strategy.asp] has a great in-depth article on this investment strategy.

Rental 30% Rule of Thumb

When renting, use the 30% rule. The rent should comprise at most 30% of your annual income. For someone making $80,000 annually, that amount would be $24,000. Therefore, someone making $80,000 annually should only rent a place that is $2,000 a month or more ($24,000 divided by 12 months).

The key to this rule of thumb is to ensure that we can afford the rent and, if possible, select a more affordable place to increase our savings and investments instead of overspending on rent. There are many opinions on how this rule is outdated since it was created in 1969. However, I believe it is a relevant rule of thumb. People may see it as irrelevant now because rents have skyrocketed, and we spend too much on rent and less on savings.

When Buying a Home, Follow the 30/30/3 Rule of Thumb.

Life insurance is crucial to ensure that we can financially protect our loved ones when we die. Life insurance is vital if we rely on an income and support someone like our partner, spouse, or children. A life insurance policy is essential because almost half of Americans could struggle financially if a wage earner in their family suddenly dies.

We may not need life insurance if we believe no one financially relies on us. However, having some life insurance for our loved ones we can leave behind may be something we want to consider.

Here are some factors to consider that could require life insurance:

The rule of thumb for life insurance is to have a policy that is 10 times our current salary.

For example, someone whose salary is $100,000 annually will require a $1 million policy. The best type of insurance to get is “term-life” insurance. Having term-life insurance may be the most cost-effective way to have life insurance. In addition, many workplaces already have life insurance coverage as a benefit. In such cases, taking out additional life insurance outside that policy to fulfill the ten times our annual salary rule of thumb may be prudent.

The FIRE (Financial Independence Retire Early) Movement is a fantastic philosophy and concept to take back the helm of work and gain financial independence from our corporate overlords.

This movement escalates the immediacy of retiring early by saving aggressively when we are young. Gone are the days of pension and our workplace taking care of us until our old age. Instead, we are left to fend for ourselves; this philosophy ensures that financial independence is the key to our freedom.

The movement is something I also follow closely and believe in as well. The FIRE movement aims to reach a certain threshold of savings and investments that could cover our expenses post-retirement amidst inflation and other factors. The idea is that we can sustain our lifestyles long past our working years. We can do this by adopting a frugal mindset to accumulate wealth that could support us long-term.

The Rule of 25

This rule of thumb is a way to measure retirement readiness. It considers one’s annual expenses and multiplies them by 25 times. So again, we need to factor in all our costs, especially needs, and essential wants. Multiply that by 12 to get our annual expense, then multiply that again by 25.

For example, if our monthly expense is $5,000 multiplied by 12, it would be an annual expense of $60,000. Multiplying that annual expense 25 times would yield a $1.5 million figure we need for retirement.

The key to streamlining the FIRE number for retirement is often lowering the annual expense. For example, for a $2,000 monthly payment, one only needs $600,000 to retire.

The 4% Rule

This rule of thumb is a way to gauge retirement sustainability. For example, a 4% drawdown on our savings and investment every year is a good accounting of the inflation of money to help our retirement last throughout our life.

The 4% rule is a way to get to a 30-year retirement goal. Retiring earlier requires our investment will have enough money to last us a lifetime. Essentially, we are living off the 4% investment from our nest egg, which requires continual support by compounding interest and market stability.

For example, for a $1 million nest egg, with the 4% rule, we need to account for the inflation rate on our first-year withdrawal. For a 5% inflation rate ($40,000 for 4% of our nest egg) equals $40,000 x 1.05, we should withdraw $42,000. This amount accounts for the inflation rate in our first year.

It is important to note that the 4% rule of thumb is a guiding principle, but we must consider the inflation rate to maintain our money’s purchasing power. This rule of thumb is due to inflation affecting the amount we could withdraw, and therefore it does affect the longevity of our nest egg. However, this 4% rule of thumb is a conservative way to ensure that our nest egg can last as long as needed.

https://youtu.be/PIBO9RvepSs?si=aFAQgjemzIPNHg5d Listen to this blog via YouTube. Right now, American educational institutions are in the…

Charlie Munger is considered one of the greatest investors of the 20th century. As a…

If you find yourself constantly stressed about money, you’re not alone. Money is one of…

As I relax on this lovely morning, I can't help but ponder on the importance…

We had a dramatic weekend, as regulators saw bank customers rushing to access their money…

When it comes to the most vital skills in personal finance, I think learning how…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}